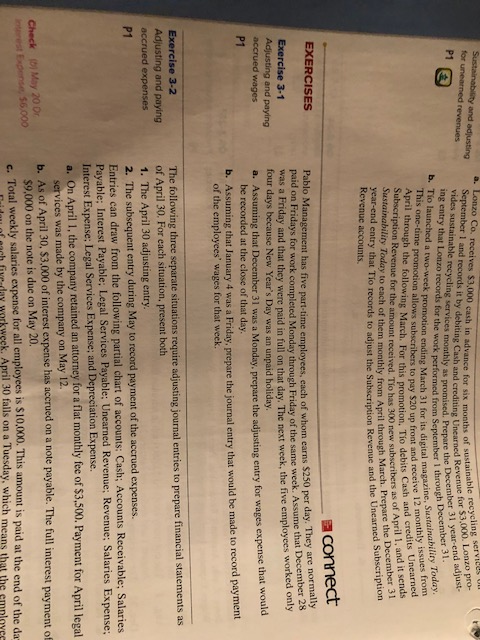

As well, envision looking at your home loan report frequently to make certain reliability. Mistakes may seem, and you will on time addressing people inaccuracies can help you maintain a clean payment record, then solidifying the creditworthiness.

The length of the financial also can enjoy a crucial role into the affecting your credit rating. Long-label loans, such as for instance a 30-seasons mortgage, join building a lengthy credit history, and therefore benefits the get over the years.

On the other hand, because you advances through the mortgage, you lower your principal balance, certainly affecting their borrowing application proportion-a switch factor in rating data. So it gradual reduction of financial obligation besides exhibits your ability so you’re able to carry out much time-term personal debt plus shows the commitment to monetary stability.

Also, keeping a home loan over a longer time may bring a good buffer facing movement on your credit score because of other financial items. As an instance, if you decide to deal with a different sort of mastercard or a consumer loan, which have a lengthy-reputation financial will help harmony your general borrowing from the bank reputation, exhibiting as you are able to manage multiple types of borrowing responsibly.

Perils and you may Cons

While you are a home loan can be certainly feeling your credit rating, this isn’t versus the risks and prospective cons. Facts this type of dangers allows greatest-advised conclusion away from homebuying. The brand new excitement of buying a home can sometimes overshadow the brand new financial obligations that are included with a home loan, so it is crucial to strategy this commitment having a definite understanding of its implications.

Dealing with financial administration that have warning will help decrease one unwanted effects on the borrowing from the bank profile. It’s important to keep in mind that a mortgage try a long-name loans, as well as the conclusion made during this time may have long-lasting impacts on your financial health. Are proactive into the wisdom their home loan small print can help your avoid problems that occur regarding mismanagement.

Whenever a mortgage Normally Reduce your Credit rating

A home loan is lower your credit history below certain circumstances. Mismanagement otherwise lost repayments is also seriously damage their score. In addition, holding high balance to the rotating borrowing from the bank shortly after taking out an excellent mortgage is adversely affect your own use proportion. So it ratio is a huge cause for credit scoring activities, and you can maintaining a low application rates is essential getting preserving an effective fit credit rating.

Likewise, by firmly taking on the a whole lot more obligations than you could potentially manage, this can raise red flags in order to loan providers, affecting your creditworthiness and you may options for upcoming credit. The pressure away https://www.cashadvancecompass.com/payday-loans-pa/ from balancing multiple expense may cause economic filter systems, it is therefore way more challenging to maintain home loan repayments. It is very important assess your general finances and make certain you to your own financial suits conveniently within your budget to eliminate the possibility getting financial distress.

Mitigating Risks toward Credit history

- Set a budget and make certain mortgage repayments complement in your financial package.

- Screen their borrowing from the bank on a regular basis to catch any issues very early.

- Have fun with equipment such as for example automated payments to eliminate later repayments.

- Restrict the newest credit inquiries to attenuate possible rating impacts.

Doing these tips might help manage your home loan effectively whenever you are securing and improving your credit score. Additionally, strengthening an emergency fund provide a financial pillow however if unanticipated costs develop, ensuring that you can meet your home loan debt rather than jeopardizing your own credit. In addition, seeking guidance off financial advisors otherwise financial masters could offer expertise tailored with the certain problem, working for you navigate the causes from home financing with certainty.

Key Takeaways and you may Advice

Basically, a home loan is also significantly connect with an individual’s credit score, one another surely and you may adversely. It presents a way to create a positive credit history, provided repayments were created promptly and you may full loans is actually treated sensibly. New perception of a home loan on your own credit score is actually multifaceted; prompt repayments can enhance your score, if you’re missed costs may cause harmful outcomes that will grab decades so you can rectify. Skills that it equilibrium is a must for everyone given home financing since the element of its economic approach.